The responsibility of saving for retirement is largely up to the individual, particularly with pensions now less commonly offered by employers. Individual retirement accounts include tax-deferred 401(k)s, 403(b)s, TSPs, and IRAs. Saving via a tax-deferred retirement account plays an important role. However, diversification is not just about the mix of investments owned but also the type of accounts owned.

There are some key benefits to accumulating a ‘bucket’ of assets in a taxable brokerage account, also referred to as an “individual” or “joint account,” that can be greatly beneficial now and in retirement.

1. More Control and Flexibility

You can contribute an unlimited amount of dollars and can withdraw funds when you want or need to.

Conversely, retirement accounts come with restrictions on how much can be contributed each year and when you can withdraw funds penalty-free. With some exceptions, these accounts are generally designed to not be used until age 59 1/2. Withdrawals before then may incur a 10 percent early withdrawal penalty.

While this rule is intended to deter accessing retirement funds for non-essential pre-retirement expenses, it also means prudent investors are restricted from withdrawing funds for a major purchase or investment without a hefty penalty.

Having a ‘bucket’ of after-tax dollars to tap for various expenses or ‘pre-retirement’ needs is crucial.

2. No Required Minimum Distributions (RMDs)

In addition to having access to brokerage account funds whenever you want, you’re also not forced to withdraw from it. With traditional tax-deferred retirement accounts, under current law you must take required minimum distributions at age 72 (some exceptions apply). Income tax is often owed on each dollar withdrawn, and the penalty for not taking the full RMD is 50 percent of the amount not distributed as required.

3. Margin Borrowing

Another possible advantage of brokerage accounts is margin – the ability to borrow against your own assets. Depending on your custodian’s margin interest rate, this can be a flexible way to access cash and potentially lower your cost of debt, while staying invested rather than selling assets. Learn more about margin here.

4. Options in a Changing Tax-Rate Environment

If income tax rates increase in the future, retirees will owe more taxes on their withdrawals from their tax-deferred accounts. Diversifying your investments by account type can provide you much needed flexibility today and in the future.

Last but not least, a Roth (or after-tax) retirement account can be an excellent way to diversify the tax structure of your investments. Some workplace 401(k) retirement plans now offer a Roth option. The contribution limits for most 401(k) plans for 2021 are $19,500, or $26,000 if age 50 or older. Contributions to a Roth IRA are limited in 2021 to $6,000, or $7,000 if age 50 or older, though higher income earners may not be eligible to contribute.

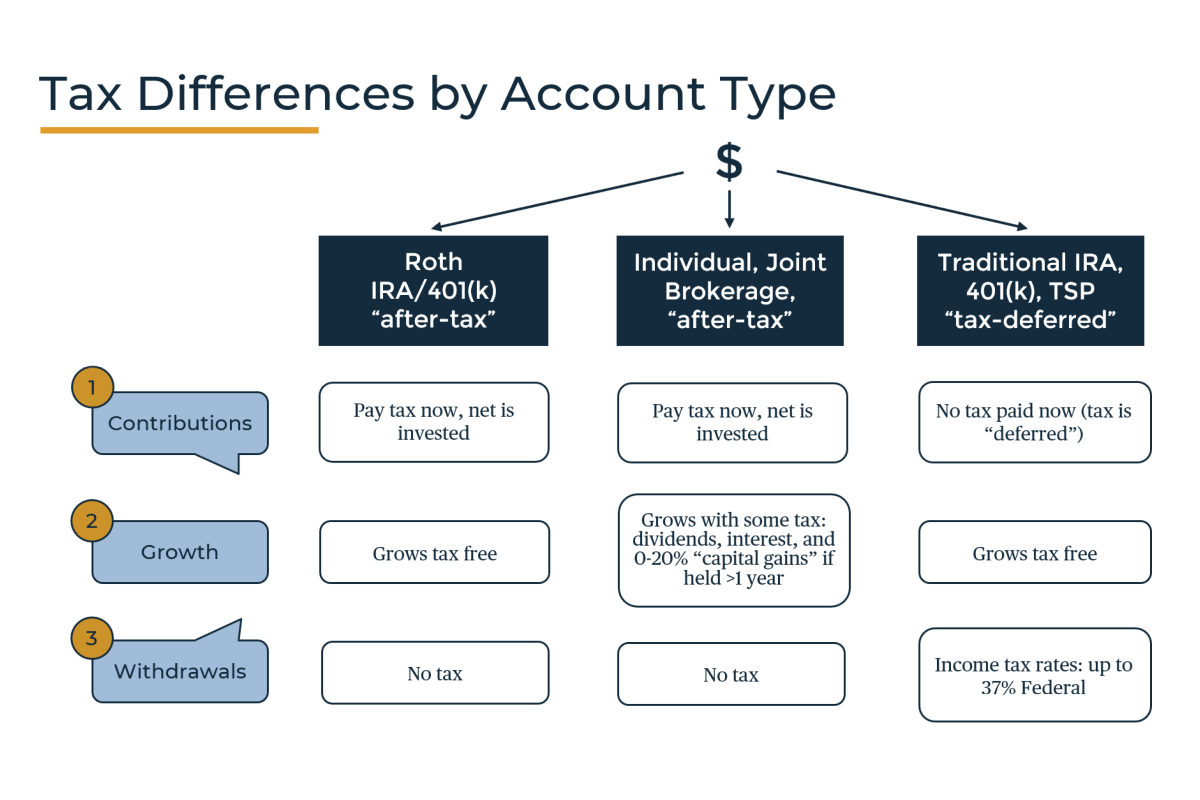

Below is a side-by-side comparison of the three main account types.

If you are interested in learning more about how much to invest in the various account types and how to streamline your income during retirement, please contact a financial advisor.

Wealthspire Advisors LLC is a registered investment adviser and subsidiary company of NFP Corp.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the certification marks CFP®, Certified Financial Planner™, and CFP® (with plaque design) in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

This information should not be construed as a recommendation, offer to sell, or solicitation of an offer to buy a particular security or investment strategy. The commentary provided is for informational purposes only and should not be relied upon for accounting, legal, or tax advice. While the information is deemed reliable, Wealthspire Advisors cannot guarantee its accuracy, completeness, or suitability for any purpose, and makes no warranties with regard to the results to be obtained from its use. © 2021 Wealthspire Advisors

This is a sponsored post. If you are interested in advertising with Northern Virginia Magazine, click here.